Entering college or university often means navigating a new financial landscape. Many students find themselves juggling tuition, textbooks, housing, and daily expenses, all while trying to establish a solid credit foundation. A well‑chosen student credit card can serve as a powerful tool—provided it carries a low interest rate that protects against costly debt accumulation.

Unlike typical credit cards marketed to the general public, student cards are designed with limited credit histories in mind. They often feature modest credit limits, educational resources, and, crucially, lower APRs that make carrying a balance less financially damaging. Understanding the nuances of student credit cards with low interest rates can empower young adults to build credit responsibly, avoid common pitfalls, and even enjoy modest rewards.

This article dives deep into the criteria for selecting the most affordable student credit cards, outlines practical strategies for maintaining a low‑interest profile, and provides actionable tips for leveraging these cards without jeopardizing financial health. Whether you’re a freshman just starting out or a senior looking to graduate with a solid credit score, the insights below will help you make informed decisions.

Key Features of Student Credit Cards with Low Interest Rates

When scouting for a student credit card with low interest rates, focus on these essential attributes:

- Annual Percentage Rate (APR): Look for cards that advertise a variable APR under 15% for purchases. Some issuers offer introductory 0% APR periods for the first 6‑12 months, which can be especially advantageous for students planning large purchases.

- Annual Fees: Most student cards waive annual fees, but verify that no hidden fees offset the low‑interest benefit.

- Credit Limit: While limits are generally modest (often $500‑$1,500), a slightly higher limit can reduce your credit utilization ratio, positively influencing your credit score.

- Rewards and Benefits: Even low‑interest cards may include cash‑back or points on categories like groceries, gas, or school supplies—just ensure the rewards don’t come with a higher APR.

- Educational Tools: Many issuers provide budgeting apps, credit monitoring, and financial literacy resources tailored for students.

How to Qualify for Student Credit Cards with Low Interest Rates

Eligibility often hinges on a combination of income, credit history, and enrollment status. Follow these steps to improve your chances:

- Demonstrate a steady source of income—part‑time jobs, scholarships, or a parent’s co‑signature can satisfy the requirement.

- Maintain a clean banking record. Overdrafts or bounced checks may raise red flags.

- Enroll as a full‑time student at an accredited institution; many issuers verify enrollment through the National Student Loan Data System (NSLDS).

- Consider applying for a secured student credit card if you have no credit history. A security deposit typically sets your credit limit and can lead to an unsecured card after responsible use.

Top Student Credit Cards with Low Interest Rates in 2024

Below is a curated list of the most competitive options currently available. All cards meet the low‑interest threshold and have been vetted for student‑friendly terms.

1. Discover it® Student Cash Back

APR: 13.99% – 23.99% variable (introductory 0% APR for the first 6 months on purchases). No annual fee. Earn 5% cash back on rotating quarterly categories up to $1,500 each quarter, and 1% on all other purchases. Discover also provides free FICO® Score monitoring and a user‑friendly mobile app.

2. Capital One Journey Student Rewards

APR: 15.24% – 25.24% variable (0% intro APR for the first 6 months). No annual fee. Offers 1% cash back on every purchase, with a boost to 1.25% when payments are made on time. The card includes automatic credit line increase reviews and an educational dashboard.

3. Bank of America® Cash Rewards for Students

APR: 14.99% – 24.99% variable (0% intro APR for the first 12 months on purchases). No annual fee. Provides 3% cash back in a category of your choice (gas, online shopping, dining, travel, drugstores, or home improvement), 2% at grocery stores, and 1% on everything else.

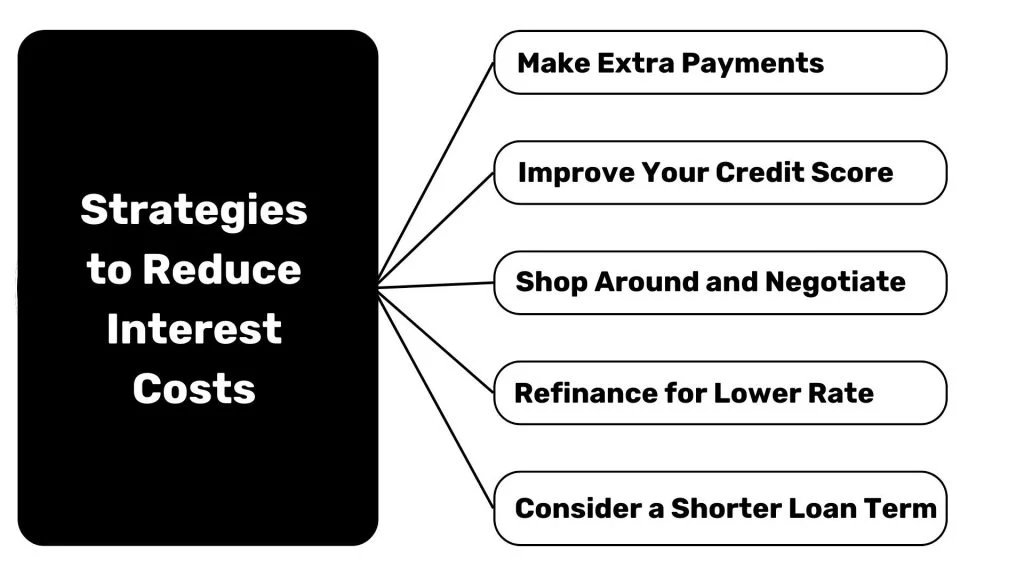

Strategies to Keep Interest Costs Low

Even the most affordable student credit cards with low interest rates can become expensive if you carry a balance. Implement these habits to protect your finances:

- Pay in Full Each Month: The simplest way to avoid interest is to clear the balance before the due date.

- Automate Payments: Set up automatic minimum payments to avoid late fees, then manually pay extra when possible.

- Utilize Introductory 0% Periods: If your card offers a 0% intro APR, plan larger purchases (like textbooks) within that window and pay them off before the rate resets.

- Monitor Your Credit Utilization: Keep utilization below 30% of your credit limit to maintain a healthy credit score.

- Negotiate a Lower Rate: After six months of on‑time payments, you can request a lower APR. For guidance, see how to negotiate lower credit card interest rates.

Student Credit Cards with Low Interest Rates vs. Regular Cards

Regular credit cards often come with higher APRs—sometimes exceeding 25%—and may require a more established credit history. In contrast, student cards prioritize accessibility and education, offering lower rates and tools that help new borrowers develop responsible habits.

Potential Pitfalls and How to Avoid Them

While low interest rates are attractive, they don’t guarantee a risk‑free experience. Be aware of these common traps:

- Late Payment Fees: Missing a due date can trigger a penalty APR, which may be significantly higher than the advertised rate.

- Over‑Limit Charges: Exceeding your credit limit can result in fees and a temporary increase in APR.

- Promotional Rate Expiration: Once the 0% intro period ends, the APR reverts to the standard rate. Keep track of the date to avoid surprise interest.

- Misunderstanding Rewards: Some cards offset low rates with high redemption thresholds. Evaluate whether the rewards truly add value.

Building Credit While Keeping Interest Low

Responsible use of a student credit card with low interest rates can jump‑start your credit profile. Follow these guidelines:

- Make at least one purchase each month and pay it off promptly.

- Keep your credit utilization under 30%—ideally below 10% for the best impact.

- Monitor your credit report annually via free services or through the issuer’s portal.

- Consider a secured credit card after graduation to transition smoothly into higher‑limit, unsecured cards.

Frequently Asked Questions

Do student credit cards really offer lower interest rates than regular cards?

Yes. Many student cards are structured with introductory 0% APR periods and variable rates that start lower than the average consumer card, which often exceeds 20% APR.

Can I qualify for a low‑interest student credit card without a co‑signer?

It’s possible if you have a steady income source (part‑time work, scholarships, or stipend) and a clean banking record. Some issuers also accept a modest security deposit for secured cards.

How long does it take to see an impact on my credit score after using a student card?

Positive activity—on‑time payments and low utilization—can be reflected in your credit score within one to two billing cycles. Consistency over six months to a year yields more substantial improvements.

What should I do if I’m charged a penalty APR?

Contact the issuer immediately, explain the situation, and request a removal. Often, demonstrating a history of on‑time payments can lead to a goodwill reversal.

Are there any student cards that combine low interest with travel rewards?

While most low‑interest student cards focus on cash back, some, like the Capital One Journey Student Rewards, provide modest points that can be transferred for travel after a few years of responsible use. For a broader view of travel‑oriented options, see the best credit cards for travel rewards – 2024 guide.

Choosing the right student credit cards with low interest rates is more than a financial decision; it’s a step toward long‑term fiscal responsibility. By evaluating APRs, fees, and benefits, and by adhering to disciplined repayment habits, students can harness these cards as a springboard to a strong credit history. Remember to review your options annually, negotiate when appropriate, and stay informed about the evolving credit landscape. With the right approach, low‑interest student cards become allies, not liabilities, on the road to financial independence.