In an increasingly digital world, credit cards have become indispensable tools for everyday transactions, from grocery shopping to booking flights. However, their convenience also makes them attractive targets for fraudsters who continuously devise new methods to exploit vulnerabilities. Understanding how to protect yourself is no longer optional; it is a fundamental part of responsible financial management.

The stakes are high. A single compromised card can lead to unauthorized purchases, a lengthy dispute process, and potential damage to your credit score. While many issuers offer robust security features, the ultimate line of defense lies with the cardholder. By adopting a proactive mindset and implementing proven safeguards, you can dramatically reduce the likelihood of falling victim to fraud.

Below, we explore a comprehensive suite of credit card fraud protection tips that blend common‑sense habits with cutting‑edge technology. Whether you’re a seasoned traveler, a student managing your first credit line, or a small‑business owner, these recommendations will help you keep your accounts secure.

Credit Card Fraud Protection Tips: Core Practices for Everyday Safety

![How to Protect Yourself from Credit Card Fraud [INFOGRAPHIC] - My Money](https://blog.jejaksemut.com/wp-content/uploads/2026/02/how-to-protect-yourself-from-credit-card-fraud-infographic-my-money-690x1024.webp)

1. Secure Your Physical Card at All Times

- Never share your PIN or card details. Treat your PIN like a password—keep it confidential and avoid writing it down.

- Use RFID‑blocking sleeves. Many modern cards contain contactless chips that can be skimmed wirelessly; a simple sleeve can prevent unauthorized reads.

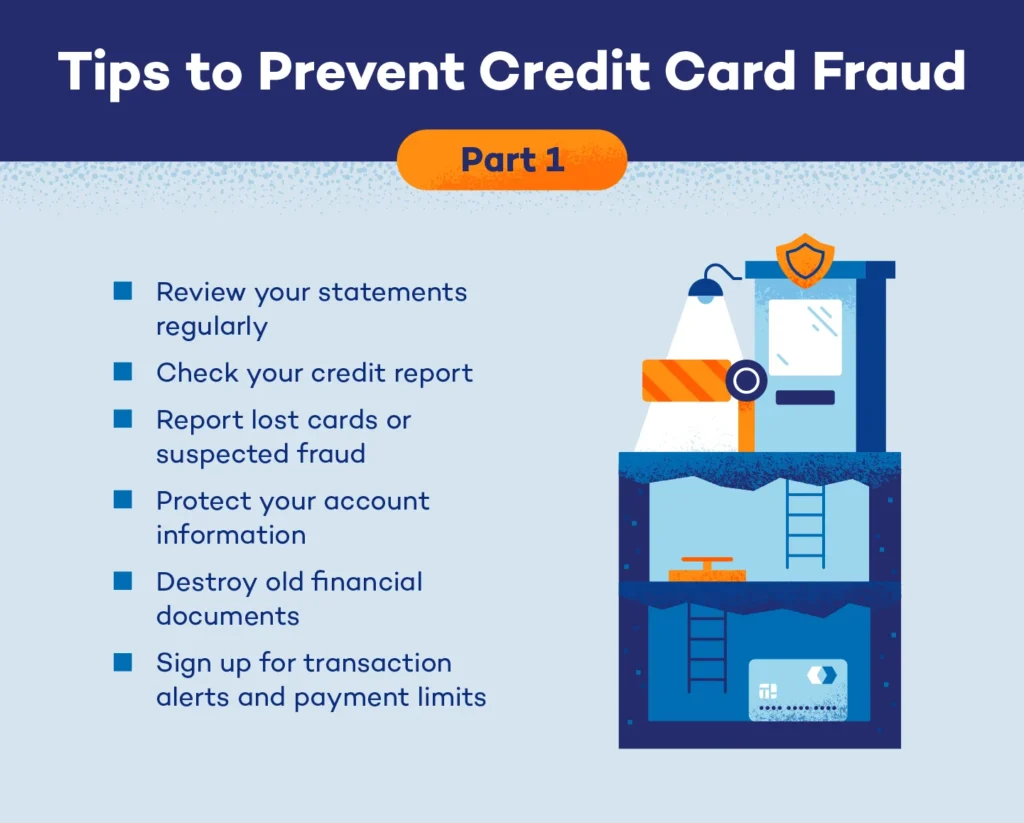

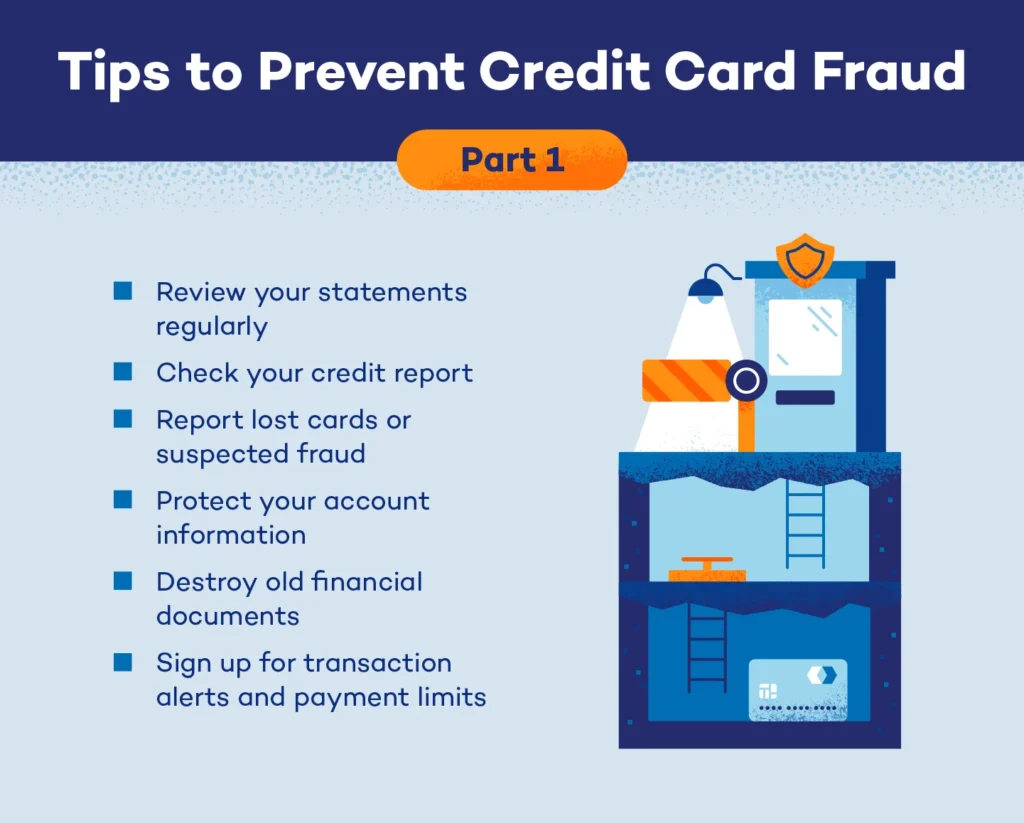

- Report lost or stolen cards immediately. Most issuers provide a 24/7 hotline; prompt reporting limits liability to as little as $0 under the Fair Credit Billing Act.

2. Leverage Built‑In Security Features

- Enable transaction alerts. Real‑time push notifications let you spot suspicious activity the moment it occurs.

- Activate virtual card numbers. Many banks issue temporary numbers for online purchases, keeping your actual card number hidden.

- Adopt two‑factor authentication (2FA). When your issuer supports it, require a second verification step—usually a text code or authenticator app—before approving changes to your account.

3. Practice Vigilant Online Shopping

- Shop only on secure (HTTPS) websites. Look for the padlock icon in the address bar before entering card details.

- Use reputable payment gateways. Platforms like PayPal or Apple Pay add an extra layer of encryption, reducing exposure of your raw card number.

- Beware of phishing emails. Phishers mimic legitimate brands to lure you into a fake login page. Verify the sender’s address and never click suspicious links.

4. Keep Software and Devices Updated

- Install security patches promptly. Outdated operating systems or browsers can harbor exploitable vulnerabilities.

- Use reputable antivirus and anti‑malware solutions. Real‑time scanning can intercept keyloggers that attempt to capture your card information.

- Enable automatic updates for mobile banking apps. Updated apps incorporate the latest fraud‑detection algorithms.

5. Monitor Statements and Credit Reports Regularly

- Review transaction history weekly. Spotting an unfamiliar charge early makes it easier to dispute.

- Set up credit monitoring alerts. Services like Experian or Credit Karma flag new inquiries or accounts opened in your name.

- Freeze your credit if you suspect identity theft. A freeze prevents new accounts from being opened without your explicit permission.

6. Use Travel‑Specific Protections Wisely

If you travel frequently, consider cards that bundle travel insurance, purchase protection, and fraud monitoring. For an in‑depth look at how travel‑related benefits can double as security safeguards, read our guide on Credit Card Travel Insurance Benefits Explained – Your Complete Guide.

7. Understand Foreign Transaction Fees and Their Impact

When using cards abroad, fraudsters often exploit currency conversion processes. Knowing the cost structure helps you spot anomalies. Our Credit Card Foreign Transaction Fees Guide breaks down the hidden fees you should watch for.

8. Choose Cards with Robust Reward and Security Synergy

Some premium cards offer real‑time fraud alerts and zero‑liability guarantees alongside generous rewards. For example, dining and entertainment cards often include purchase protection that covers unauthorized transactions. Learn more in the Best Credit Cards for Dining and Entertainment: A 2024 Guide.

Advanced Credit Card Fraud Protection Tips for Tech‑Savvy Users

Utilize Tokenization and Mobile Wallets

Tokenization replaces your card number with a random token during each transaction. Mobile wallets like Google Pay and Apple Pay automatically apply this technology, ensuring that merchants never see your actual account details.

Set Custom Spending Limits

Many issuers allow you to define daily or per‑transaction caps. By setting a low limit for online purchases, you minimize potential loss if a fraudster gains access to your card.

Employ a Dedicated Email for Financial Accounts

Segregating your banking communications to a separate, strongly protected email address reduces exposure to credential‑stuffing attacks.

Consider a Credit Freeze on Unused Cards

If you have multiple cards but use only a few regularly, placing a temporary freeze on the dormant ones can prevent fraudsters from activating them without your knowledge.

Credit Card Fraud Protection Tips: What to Do If You Suspect Fraud

Immediate Actions

- Contact your card issuer’s fraud hotline—most provide a toll‑free number reachable 24/7.

- Lock or cancel the compromised card via the issuer’s mobile app to stop further transactions.

- Document the incident: note dates, amounts, merchant names, and any suspicious communications.

Dispute Process Overview

Under the Fair Credit Billing Act, you have 60 days from the statement date to dispute a charge. Submit a written statement to your issuer, attach supporting evidence, and keep copies for your records. Most banks will provisionally credit the amount while investigating.

Rebuilding After Fraud

- Review and update all passwords linked to financial services.

- Consider a credit‑monitoring subscription for the next 12‑24 months.

- Re‑evaluate your security settings—enable additional alerts, tighten 2FA, and perhaps adopt a different card for online use.

Future Trends in Credit Card Fraud Protection

Artificial Intelligence and Machine Learning

Issuers are increasingly employing AI to detect anomalous spending patterns in real time. These systems can flag a transaction that deviates from your usual behavior—such as a high‑value purchase in a foreign country—before it’s authorized.

Biometric Authentication

Fingerprints, facial recognition, and voice verification are becoming standard for mobile payments, adding a personal identifier that’s far harder to replicate than a password.

Blockchain‑Based Verification

Emerging blockchain solutions promise immutable transaction records, making it virtually impossible for fraudsters to alter or counterfeit purchase data.

While technology will continue to evolve, the foundation of credit card fraud protection remains the same: vigilance, timely action, and leveraging the tools your issuer provides. By integrating the above credit card fraud protection tips into your daily routine, you not only safeguard your finances but also reinforce a culture of security that can protect you for years to come.

Frequently Asked Questions

What is the most effective credit card fraud protection tip?

Enabling real‑time transaction alerts and promptly reviewing your statements are often cited as the quickest way to detect unauthorized activity before significant damage occurs.

Can virtual card numbers prevent fraud?

Yes. Virtual numbers generate a temporary card identifier for each online purchase, keeping your actual card number concealed and reducing exposure to data breaches.

Do I need a separate password for each credit card account?

Ideally, yes. Using unique, strong passwords for each financial account limits the risk of a single compromised credential granting access to multiple cards.

How does a credit freeze differ from a fraud alert?

A fraud alert notifies lenders to verify your identity before opening new credit, while a credit freeze blocks all new credit inquiries entirely until you lift the freeze.

Is it safe to store my card details in my phone’s wallet?

Mobile wallets use tokenization and biometric locks, making them generally more secure than storing raw card numbers in plain text.

Staying ahead of fraudsters requires a combination of common‑sense habits, awareness of emerging threats, and active use of the security tools your card issuer offers. By committing to these credit card fraud protection tips, you can enjoy the convenience of modern payment methods without compromising your financial wellbeing.